The private label landscape is experiencing unprecedented growth and transformation across retail channels. With all the news around private label performance, various new brand launches last year, and recent tariff concerns, and the buzz at PLMA in Chicago, the Harvest Group team decided to pause and reflect on how businesses at Walmart, Target, and Amazon were impacted in 2024.

Here’s a comprehensive look at the current state of private label and what’s driving its success.

Private Label Market Overview: Store Brands Breaking Records in 2024

Store brands reached all-time highs in both unit and dollar share during the first half of 2024, capturing approximately 23% of unit market share and 20% of dollar share according to the PLMA and Circana. The trajectory suggests potential for some U.S. retailers to reach as high as 40%+ in the coming years.

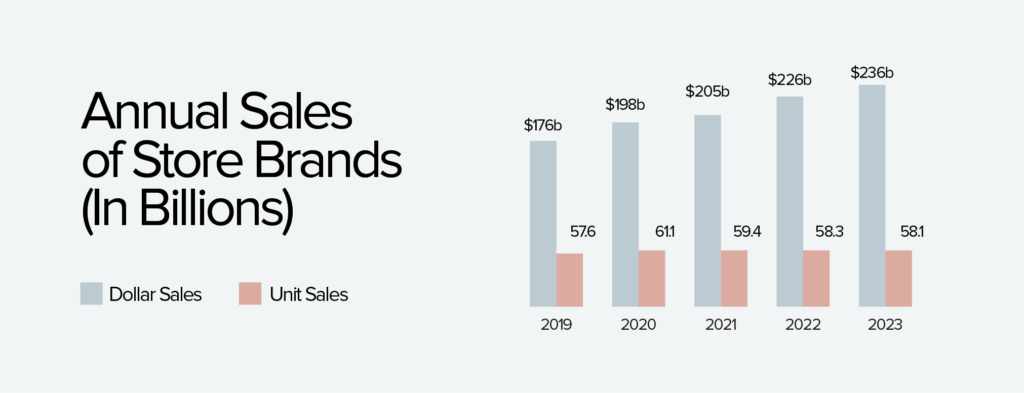

Annual Store Brand Sales Growth:

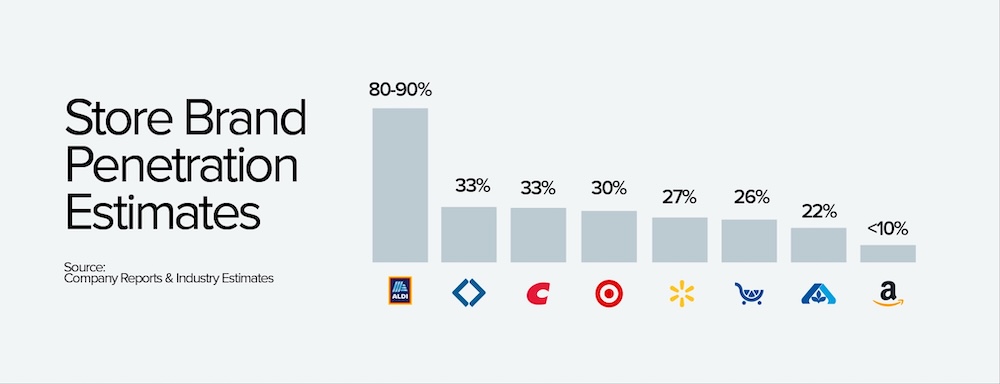

Market Penetration

Value retailers and club stores are leading the private label charge, with both Sam’s Club and Costco reaching 33% penetration rates. This success demonstrates consumers’ growing trust in store brands, particularly in bulk and value-oriented shopping environments. The full retail landscape shows varying degrees of sales penetration:

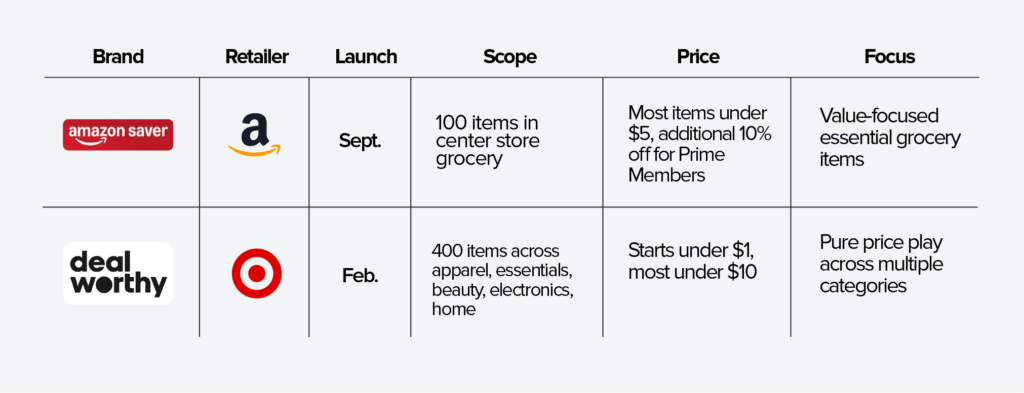

Notable 2024 Private Label Launches

Premium Tier

Value Focus

Market Drivers and Trends

Economic Factors

Multi-year food inflation and a cautious consumer environment have accelerated private label adoption and innovation. This has prompted retailers to refresh their private label strategies and invest in new brand development.

Supply Chain Considerations

A significant portion of store brand goods are manufactured outside the U.S., leading retailers to diversify their production sources and enhance supply chain transparency in the anticipation of additional tariffs.

Pricing Dynamics

As inflation has begun to abate, retailers are leveraging private label offerings in their pricing strategies, often leading with these brands in price reductions, hoping brands will follow suit.

Looking Ahead – 2025 Outlook for Private Label and Store Brands

The private label sector appears poised for continued growth into 2025, with retailers investing heavily in brand development and portfolio management. The evolution from simple price plays to sophisticated brand strategies suggests store brands will continue to gain market share and consumer trust.

“Private label always makes headlines during inflationary times, but this time does feel a little different. Momentum is poised to carry on in 2025 even with more economic stability as retailers have cracked the code on quality + differentiation and more brands have adopted an ‘and’ vs. ‘or’ strategy to win.”

Are you manufacturing private label products and need help navigating your retail partnerships? Struggling to compete with private label and need advice? Reach out to us at hello@harvestgroup.com or fill out our Contact Us form.